YIELD (CURVE) WATCH

BNY Investment's Global Economic and Investment Analysis team offers a snapshot of today’s yield curve and what it means for asset classes and investment opportunities.

BNY Investment's Global Economic and Investment Analysis team offers a snapshot of today’s yield curve and what it means for asset classes and investment opportunities.

Time to Read: 3 minutes

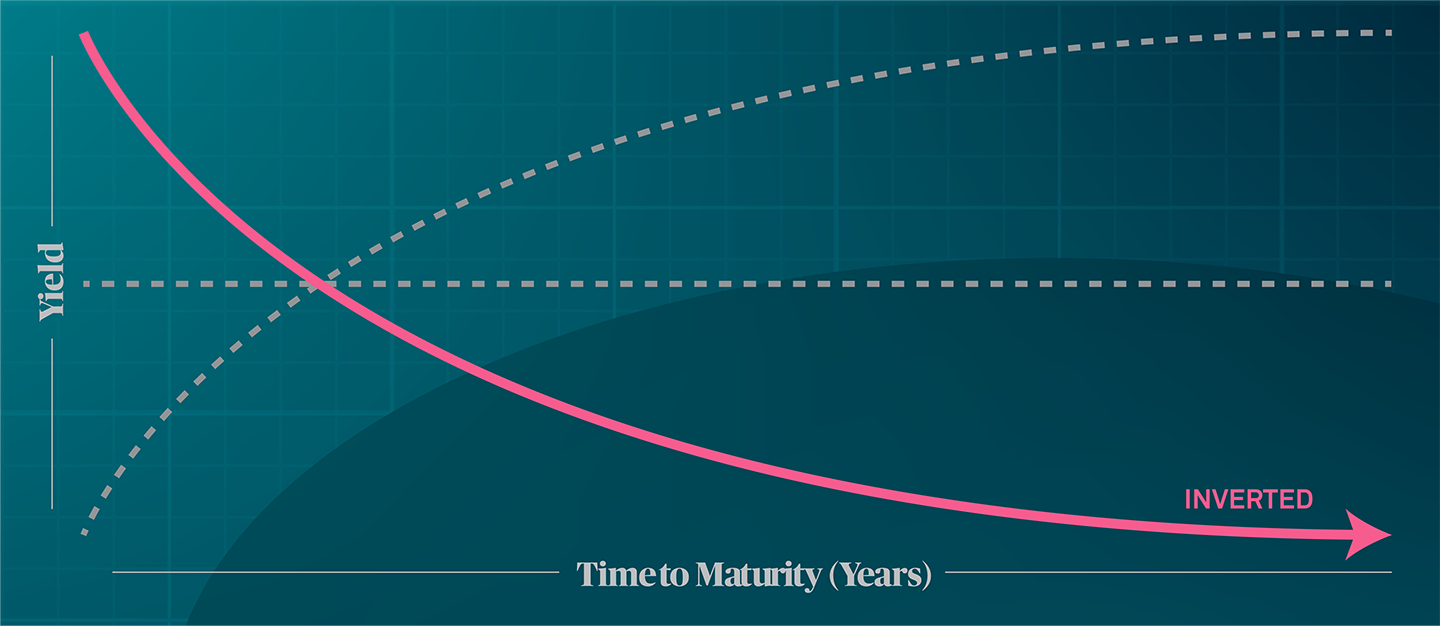

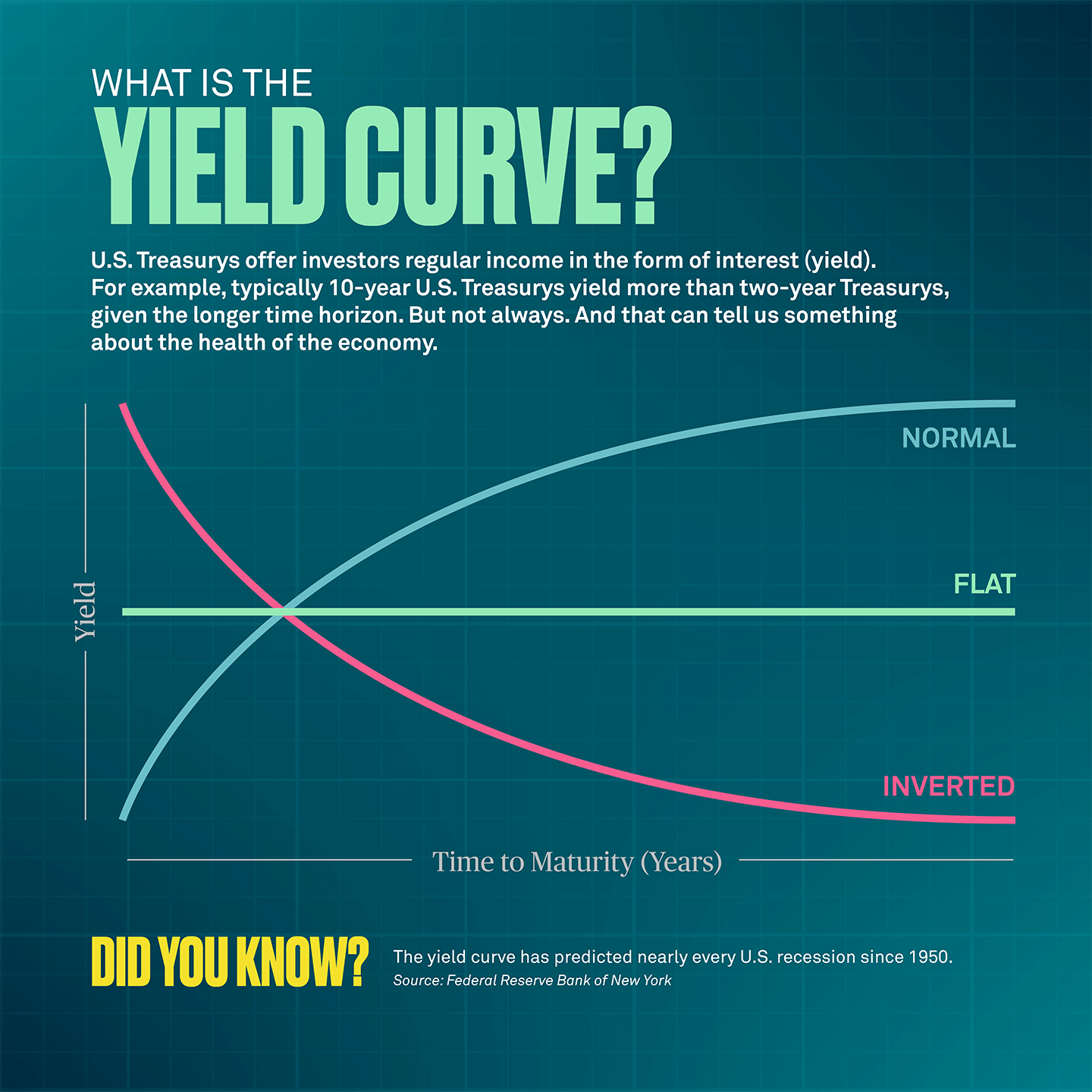

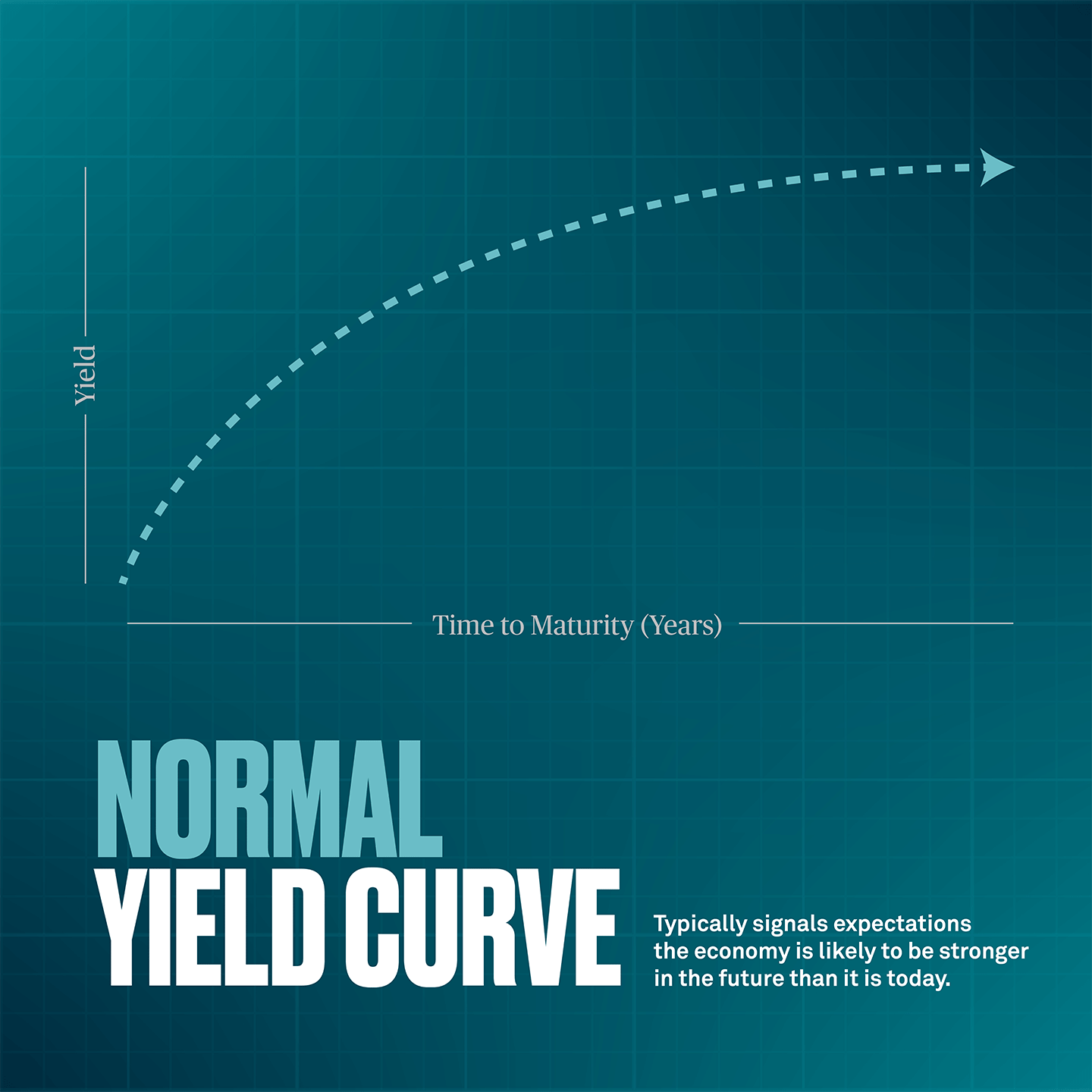

The yield curve (2s10s) may still be inverted, indicating the yield on two-year Treasurys is currently higher than 10-year Treasuries, but a steepening may soon change that. The inverted position of the curve – which typically precedes a recession – looks to be moving after an unusually long period (since July 2022).

The Federal Reserve shifted their monetary policy and hiked interest rates aggressively to control inflation (2022/2023). Borrowing costs increased particularly in the short end of the curve as investors priced in a period of elevated inflation and restrictive policy, but with expectations for a normalization in both for the years ahead.

A steepening of the yield curve usually hints at an impending economic slowdown or recession. But this time has been somewhat different. Investors appear to be pricing in a stronger long-term rate of growth for the U.S. economy (a so-called bear steepening).

While a further steepening of the yield curve is the most likely scenario, the underlying reason matters a great deal for investors. A bear steepening tends to favor riskier assets, like equities.

In recent months, the U.S. yield curve has started to steepen (becoming less negative) from previously very inverted levels.

This is being driven by long-term Treasury yields moving higher and short-term interest rates falling a little. While the yield curve may remain somewhat volatile over the coming months, a further steepening is the most likely path from here.

BNY's iFlow "Mood" Index, tracking investor flows across equities and bonds, is trending up after hitting its lowest point since the pandemic, signaling a resilient U.S. economy in 2025. Across the globe, opportunities for growth are mixed but setting the stage for incoming governments to pursue pro-growth policies via private sector funding.

Learn how EU leaders are working to develop a continental capital markets union that could reinvigorate the European economy.

The market for private credit has grown tenfold since 2007 and is projected to hit $3.5 trillion by 2028. This explosive growth is attracting not only new pockets of capital, including retail investors, but also scrutiny over potential financial stability concerns.

Distribution, fees, transparency and market structure are key challenges in the rapidly growing active exchange-traded funds (ETF) market in Europe, according to a panel hosted by BNY.

BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. This material does not constitute a recommendation by BNY Mellon of any kind. The information herein is not intended to provide tax, legal, investment, accounting, financial or other professional advice on any matter, and should not be used or relied upon as such. The views expressed within this material are those of the contributors and not necessarily those of BNY Mellon. BNY Mellon has not independently verified the information contained in this material and makes no representation as to the accuracy, completeness, timeliness, merchantability or fitness for a specific purpose of the information provided in this material. BNY Mellon assumes no direct or consequential liability for any errors in or reliance upon this material.